Delfi Ltd

SGX:P34

| US |

|

Johnson & Johnson

NYSE:JNJ

|

Pharmaceuticals

|

| US |

|

Berkshire Hathaway Inc

NYSE:BRK.A

|

Financial Services

|

| US |

|

Bank of America Corp

NYSE:BAC

|

Banking

|

| US |

|

Mastercard Inc

NYSE:MA

|

Technology

|

| US |

|

UnitedHealth Group Inc

NYSE:UNH

|

Health Care

|

| US |

|

Exxon Mobil Corp

NYSE:XOM

|

Energy

|

| US |

|

Pfizer Inc

NYSE:PFE

|

Pharmaceuticals

|

| US |

|

Palantir Technologies Inc

NYSE:PLTR

|

Technology

|

| US |

|

Nike Inc

NYSE:NKE

|

Textiles, Apparel & Luxury Goods

|

| US |

|

Visa Inc

NYSE:V

|

Technology

|

| CN |

|

Alibaba Group Holding Ltd

NYSE:BABA

|

Retail

|

| US |

|

JPMorgan Chase & Co

NYSE:JPM

|

Banking

|

| US |

|

Coca-Cola Co

NYSE:KO

|

Beverages

|

| US |

|

Walmart Inc

NYSE:WMT

|

Retail

|

| US |

|

Verizon Communications Inc

NYSE:VZ

|

Telecommunication

|

| US |

|

Chevron Corp

NYSE:CVX

|

Energy

|

Utilize notes to systematically review your investment decisions. By reflecting on past outcomes, you can discern effective strategies and identify those that underperformed. This continuous feedback loop enables you to adapt and refine your approach, optimizing for future success.

Each note serves as a learning point, offering insights into your decision-making processes. Over time, you'll accumulate a personalized database of knowledge, enhancing your ability to make informed decisions quickly and effectively.

With a comprehensive record of your investment history at your fingertips, you can compare current opportunities against past experiences. This not only bolsters your confidence but also ensures that each decision is grounded in a well-documented rationale.

Do you really want to delete this note?

This action cannot be undone.

| 52 Week Range |

0.67

0.905

|

| Price Target |

|

We'll email you a reminder when the closing price reaches SGD.

Choose the stock you wish to monitor with a price alert.

|

|

Johnson & Johnson

NYSE:JNJ

|

US |

|

|

Berkshire Hathaway Inc

NYSE:BRK.A

|

US |

|

|

Bank of America Corp

NYSE:BAC

|

US |

|

|

Mastercard Inc

NYSE:MA

|

US |

|

|

UnitedHealth Group Inc

NYSE:UNH

|

US |

|

|

Exxon Mobil Corp

NYSE:XOM

|

US |

|

|

Pfizer Inc

NYSE:PFE

|

US |

|

|

Palantir Technologies Inc

NYSE:PLTR

|

US |

|

|

Nike Inc

NYSE:NKE

|

US |

|

|

Visa Inc

NYSE:V

|

US |

|

|

Alibaba Group Holding Ltd

NYSE:BABA

|

CN |

|

|

JPMorgan Chase & Co

NYSE:JPM

|

US |

|

|

Coca-Cola Co

NYSE:KO

|

US |

|

|

Walmart Inc

NYSE:WMT

|

US |

|

|

Verizon Communications Inc

NYSE:VZ

|

US |

|

|

Chevron Corp

NYSE:CVX

|

US |

This alert will be permanently deleted.

Intrinsic Value

The intrinsic value of one P34 stock under the Base Case scenario is hidden SGD. Compared to the current market price of 0.79 SGD, Delfi Ltd is hidden .

The Intrinsic Value is calculated as the average of DCF and Relative values:

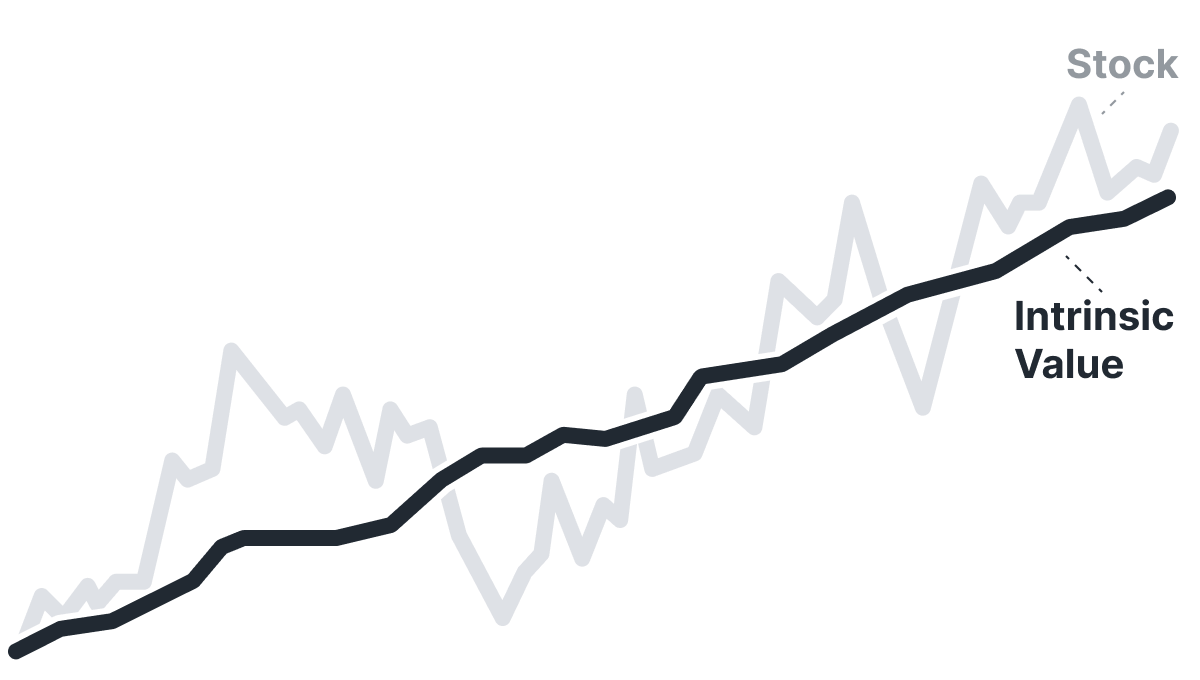

Valuation History

Delfi Ltd

P34 looks undervalued. But is it really? Some stocks live permanently below intrinsic value; one glance at Historical Valuation reveals if P34 is one of them.

Learn how current stock valuations stack up against historical averages to gauge true investment potential.

Let our AI compare Alpha Spread’s intrinsic value with external valuations from Simply Wall St, GuruFocus, ValueInvesting.io, Seeking Alpha, and others.

Let our AI break down the key assumptions behind the intrinsic value calculation for Delfi Ltd.

| JP |

G

|

Goyo Foods Industry Co Ltd

TSE:2230

|

|

| CH |

|

Nestle SA

SIX:NESN

|

|

| US |

|

Mondelez International Inc

NASDAQ:MDLZ

|

|

| ZA |

T

|

Tiger Brands Ltd

JSE:TBS

|

|

| FR |

|

Danone SA

PAR:BN

|

|

| MY |

O

|

Ocb Bhd

KLSE:OCB

|

|

| US |

|

Hershey Co

NYSE:HSY

|

|

| CN |

|

Muyuan Foods Co Ltd

SZSE:002714

|

|

| ZA |

A

|

Avi Ltd

JSE:AVI

|

|

| CH |

|

Chocoladefabriken Lindt & Spruengli AG

SIX:LISN

|

Fundamental Analysis

Select up to 3 indicators:

Select up to 3 indicators:

Revenue & Expenses Breakdown

Delfi Ltd

Balance Sheet Decomposition

Delfi Ltd

| Current Assets | 307.2m |

| Cash & Short-Term Investments | 81.6m |

| Receivables | 114.5m |

| Other Current Assets | 111.1m |

| Non-Current Assets | 138.7m |

| Long-Term Investments | 2.6m |

| PP&E | 106.6m |

| Intangibles | 18.3m |

| Other Non-Current Assets | 11.2m |

| Current Liabilities | 161.2m |

| Accounts Payable | 46.5m |

| Short-Term Debt | 20m |

| Other Current Liabilities | 94.7m |

| Non-Current Liabilities | 14.1m |

| Other Non-Current Liabilities | 14.1m |

Free Cash Flow Analysis

Delfi Ltd

| USD | |

| Free Cash Flow | USD |

Earnings Waterfall

Delfi Ltd

|

Revenue

|

501.4m

USD

|

|

Cost of Revenue

|

-367.4m

USD

|

|

Gross Profit

|

134m

USD

|

|

Operating Expenses

|

-93.1m

USD

|

|

Operating Income

|

40.9m

USD

|

|

Other Expenses

|

-14.3m

USD

|

|

Net Income

|

26.6m

USD

|

P34 Profitability Score

Profitability Due Diligence

Delfi Ltd's profitability score is hidden . The higher the profitability score, the more profitable the company is.

Score

Delfi Ltd's profitability score is hidden . The higher the profitability score, the more profitable the company is.

P34 Solvency Score

Solvency Due Diligence

Delfi Ltd's solvency score is hidden . The higher the solvency score, the more solvent the company is.

Score

Delfi Ltd's solvency score is hidden . The higher the solvency score, the more solvent the company is.

Wall St

Price Targets

P34 Price Targets Summary

Delfi Ltd

According to Wall Street analysts, the average 1-year price target for P34 is 0.86 SGD with a low forecast of 0.81 SGD and a high forecast of 0.99 SGD.

Dividends

Current shareholder yield for P34 is hidden .

Shareholder yield represents the total return a company provides to its shareholders, calculated as the sum of dividend yield, buyback yield, and debt paydown yield. What is shareholder yield?

The intrinsic value of one P34 stock under the Base Case scenario is hidden SGD.

Compared to the current market price of 0.79 SGD, Delfi Ltd is hidden .