Krung Thai Bank PCL

SET:KTB

Utilize notes to systematically review your investment decisions. By reflecting on past outcomes, you can discern effective strategies and identify those that underperformed. This continuous feedback loop enables you to adapt and refine your approach, optimizing for future success.

Each note serves as a learning point, offering insights into your decision-making processes. Over time, you'll accumulate a personalized database of knowledge, enhancing your ability to make informed decisions quickly and effectively.

With a comprehensive record of your investment history at your fingertips, you can compare current opportunities against past experiences. This not only bolsters your confidence but also ensures that each decision is grounded in a well-documented rationale.

Do you really want to delete this note?

This action cannot be undone.

| 52 Week Range |

15.5

21.7

|

| Price Target |

|

We'll email you a reminder when the closing price reaches THB.

Choose the stock you wish to monitor with a price alert.

This alert will be permanently deleted.

Krung Thai Bank PCL

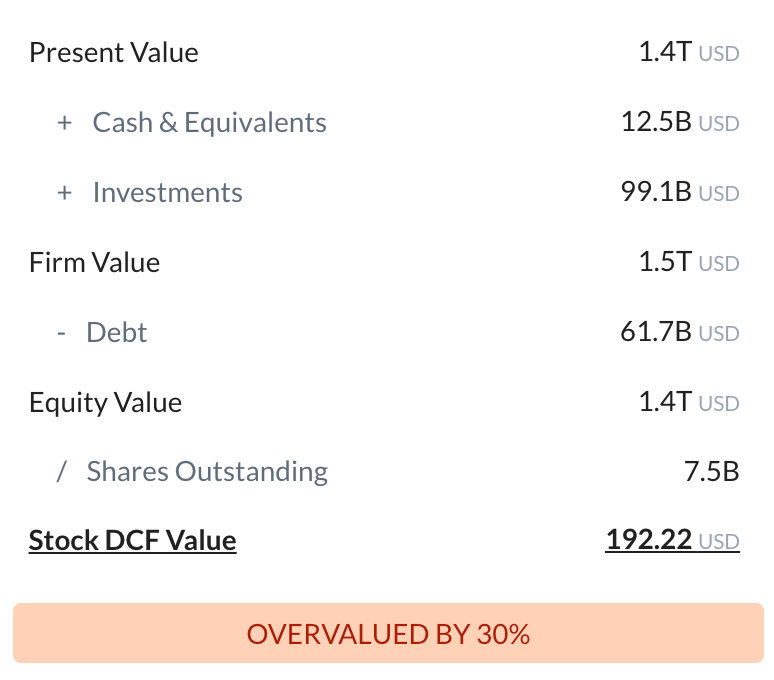

Intrinsic Value

The intrinsic value of one

KTB

stock under the Base Case scenario is

43.84

THB.

Compared to the current market price of 20.3 THB,

Krung Thai Bank PCL

is

Undervalued by 54%.

The Intrinsic Value is calculated as the average of DCF and Relative values:

Valuation Backtest

Krung Thai Bank PCL

Uncover deeper insights with the Valuation Backtest. Learn how current stock valuations stack up against historical averages to gauge true investment potential.

Start backtest now and learn if your stock is truly undervalued or overvalued!

Stock is trading at its lowest valuation over the past 5 years.

To access the results of this valuation backtest, please register an account with us. Registration is quick and gives you instant access to insights on 3 stocks per week for free.

The backtest for KTB cannot be conducted due to limitations such as insufficient data or other constraints. Please select a different stock or adjust your settings.

Fundamental Analysis

Economic Moat

Krung Thai Bank PCL

Select up to 3 indicators:

Select up to 3 indicators:

Months

Months

Months

Months

Select up to 2 periods:

Krung Thai Bank PCL, a leading financial institution in Thailand, has made a name for itself as a pillar of stability and innovation in the banking sector. Established in 1966, the bank offers a comprehensive range of services, including retail banking, corporate finance, investment services, and asset management. With a robust network of branches and digital platforms extending across the nation, Krung Thai Bank has become a trusted partner for millions of customers, small businesses, and large corporations alike. The bank's commitment to customer service and sustainable practices positions it well in the evolving landscape of finance, especially amid increasing competition and the rapid sh...

Krung Thai Bank PCL, a leading financial institution in Thailand, has made a name for itself as a pillar of stability and innovation in the banking sector. Established in 1966, the bank offers a comprehensive range of services, including retail banking, corporate finance, investment services, and asset management. With a robust network of branches and digital platforms extending across the nation, Krung Thai Bank has become a trusted partner for millions of customers, small businesses, and large corporations alike. The bank's commitment to customer service and sustainable practices positions it well in the evolving landscape of finance, especially amid increasing competition and the rapid shift towards digital solutions.

Investors eyeing Krung Thai Bank will find a company that boasts a solid financial foundation, with consistent profitability and prudent risk management strategies. The bank has shown resilience through economic fluctuations, leveraging its diverse portfolio to minimize risks while maximizing growth opportunities. With a focus on technological innovation and enhancing customer experiences, Krung Thai Bank is not just keeping pace with industry trends but is also setting the benchmark for others in the region. As the bank continues to expand its digital offerings and strengthen its market presence, it stands poised for future growth, making it an appealing option for those looking to invest in a dynamic and well-established financial entity.

Krung Thai Bank Public Company Limited (KTB), one of Thailand's leading financial institutions, primarily operates in several core business segments:

-

Retail Banking: This segment provides a wide range of banking services to individual customers, including savings accounts, personal loans, home loans, and credit cards. KTB focuses on offering customer-centric products and services aimed at enhancing customer experience and satisfaction.

-

Corporate Banking: KTB serves large and medium-sized businesses with various financial products, including corporate loans, trade finance, treasury and cash management services, and investment banking solutions. This segment helps companies manage their financial needs and supports their growth strategies.

-

SME Banking: The bank offers specialized products and services tailored for small and medium-sized enterprises. These include working capital loans, business loans, and advisory services aimed at helping SMEs overcome financial challenges and stimulate growth.

-

Wholesale Banking: This segment focuses on providing comprehensive banking services to institutional clients. Services include syndicated loans, project financing, foreign exchange, and treasury products, helping large organizations manage their complex financial needs.

-

Investment Banking: KTB engages in various investment banking activities, such as mergers and acquisitions advisory, underwriting, and capital raising services. This segment is aimed at both corporations and government entities seeking to maximize their financial operations.

-

Islamic Banking: KTB provides Islamic financial products that comply with Sharia law, catering to customers who prefer such financial solutions. The bank offers a range of services including Islamic savings accounts, investment products, and financing options.

-

Wealth Management: This segment caters to high-net-worth individuals and offers personalized financial advisory services, investment management, and estate planning to help clients grow and preserve their wealth.

-

Digital Banking: KTB is focusing on enhancing its digital banking capabilities, offering applications and platforms for online banking, mobile payments, and other fintech solutions, which aim to improve accessibility and convenience for customers.

These segments allow Krung Thai Bank to diversify its offerings and create a comprehensive portfolio of financial services, appealing to a wide range of customers from individuals to large corporations.

Krung Thai Bank PCL (KTB) holds several unique competitive advantages that help it stand out in the competitive landscape of banking in Thailand. Here are some key advantages:

-

Government Ownership and Support: As a state-owned bank, KTB benefits from implicit government backing. This can enhance its stability and credibility, attracting more customers and ensuring trust, especially in times of financial uncertainty.

-

Extensive Branch Network: KTB has one of the largest branch networks in Thailand, making banking accessible to a wide range of customers, including those in rural areas. This extensive presence helps facilitate customer acquisition and relationship management.

-

Focus on Retail Banking and SMEs: KTB has a strong focus on retail banking and small and medium-sized enterprises (SMEs), which are crucial segments in the Thai economy. This specialization allows KTB to tailor its products and services effectively to meet the needs of these customers.

-

Innovative Digital Banking Solutions: KTB has been investing in digital banking technologies, enhancing its online and mobile banking platforms. This pivot towards digitalization not only improves customer service but also operational efficiency, attracting tech-savvy customers.

-

Strong Brand Recognition: With its long history and strong market presence, KTB enjoys high brand recognition. This is crucial in the banking sector, where trust and reputation significantly influence customer choice.

-

Diverse Product Offerings: KTB provides a wide range of financial products and services, including personal loans, mortgages, savings accounts, investment products, and corporate banking services. This diversification helps KTB capture various market segments and cross-sell products.

-

Risk Management and Regulatory Compliance: KTB's experience and established risk management protocols allow it to navigate regulatory environments effectively. This is particularly important in maintaining stability and compliance in a highly regulated industry.

-

Community Engagement and Social Responsibility: The bank’s initiatives in corporate social responsibility can enhance its reputation and local engagement, helping build long-term customer relationships rooted in community support.

-

Strategic Partnerships and Collaborations: KTB has opportunities for partnerships with fintech companies and other financial entities, leveraging technology to enhance service delivery and expand offerings.

By leveraging these advantages, Krung Thai Bank can position itself effectively against its rivals while continuing to grow its market share and enhance customer loyalty.

As a prominent financial institution in Thailand, Krung Thai Bank PCL faces several risks and challenges in the near future. Here are some critical factors to consider:

-

Economic Factors:

- Economic Slowdown: A slowdown in Thailand’s economy, possibly due to global economic conditions, can lead to reduced lending opportunities and increased non-performing loans.

- Inflation: Rising inflation can erode purchasing power and impact consumer spending, leading to reduced demand for loans and financial services.

-

Regulatory Challenges:

- Compliance Costs: Increasing regulatory requirements can lead to higher compliance costs, which may affect profitability.

- Changes in Banking Regulations: New regulations regarding capital requirements, lending practices, and consumer protection can impose additional operational challenges.

-

Technological Disruption:

- Fintech Competition: The rise of fintech companies poses a significant challenge, impacting traditional banking through competitive products and services.

- Cybersecurity Risks: As digital banking grows, so does the risk of cyber attacks, which can lead to significant financial losses and damage to reputation.

-

Market Competition:

- Intense Competition: The banking sector in Thailand is highly competitive, with numerous banks vying for market share. This can lead to pricing pressures and reduced margins on loans and financial products.

-

Credit Risks:

- Loan Defaults: An increase in defaults, especially from SMEs and consumer loans, can negatively impact the bank’s financial health.

- Sector Exposure: High exposure to certain sectors (e.g., real estate, tourism) that may be vulnerable to economic downturns can increase credit risks.

-

Political and Social Factors:

- Political Instability: Political uncertainty or instability in Thailand can affect economic performance and banking operations.

- Social Unrest: Any social unrest or public discontent can lead to increased operational risks and impact customer sentiment.

-

Interest Rate Fluctuations:

- Rising Interest Rates: If interest rates rise, there may be increased borrowing costs for consumers and businesses, leading to potential declines in loan growth.

-

Foreign Exchange Risks:

- Currency Volatility: As a bank with international operations, fluctuations in foreign exchange rates can impact profitability and risk management.

-

Pandemic Aftereffects:

- Long-term Effects of COVID-19: The lingering economic effects of the pandemic, including changes in consumer behavior and business operations, can pose challenges for traditional banking models.

-

Environmental Risks:

- Sustainability Concerns: Increasing focus on environmental, social, and governance (ESG) factors may influence investment decisions and regulatory expectations.

To mitigate these risks, Krung Thai Bank will need to adopt a proactive risk management strategy, invest in technology, and continuously adapt to the evolving financial landscape.

Balance Sheet Decomposition

Krung Thai Bank PCL

| Net Loans | 2.4T |

| Investments | 969.5B |

| PP&E | 33B |

| Intangibles | 20.1B |

| Other Assets | 249B |

| Total Deposits | 2.9T |

| Long Term Debt | 139.5B |

| Other Liabilities | 203.6B |

Wall St

Price Targets

KTB Price Targets Summary

Krung Thai Bank PCL

According to Wall Street analysts, the average 1-year price target for

KTB

is 23.51 THB

with a low forecast of 18.28 THB and a high forecast of 27.3 THB.

Dividends

Current shareholder yield for KTB is

.

Shareholder yield represents the total return a company provides to its shareholders, calculated as the sum of dividend yield, buyback yield, and debt paydown yield. What is shareholder yield?

Profile

Krung Thai Bank PCL

Country

Industry

Market Cap

Dividend Yield

Description

Krung Thai Bank Public Co., Ltd. engages in the provision of commercial banking services. The company is headquartered in Bangkok, Bangkok Metropolis and currently employs 18,937 full-time employees. The Bank is organized into three business segments: retail banking segment, which relates to the development of financial products and services and the provision of services for individual customers, such as deposits, loans, payment for goods and services, as well as sale of products; wholesale banking segment including the provision of credit facilities and financial services to corporate clients, and treasury and investment segment, which focuses on controlling the Bank’s financial structure, making profit from the Bank’s equity investment, foreign currency exchange services, international business and excess liquidity, and also supervising overseas branches and companies in which the Bank has invested.

Contact

IPO

Employees

Officers

The intrinsic value of one

KTB

stock under the Base Case scenario is

43.84

THB.

Compared to the current market price of 20.3 THB,

Krung Thai Bank PCL

is

Undervalued by 54%.

You don't have any saved screeners yet

You don't have any saved screeners yet