Warrior Met Coal Inc

NYSE:HCC

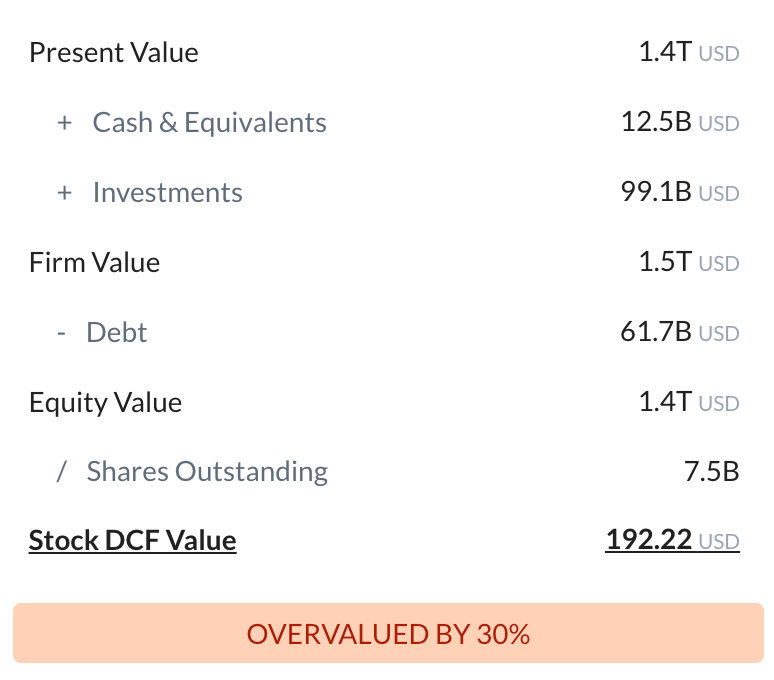

Intrinsic Value

The intrinsic value of one

HCC

stock under the Base Case scenario is

71.9

USD.

Compared to the current market price of 49.35 USD,

Warrior Met Coal Inc

is

Undervalued by 31%.

The Intrinsic Value is calculated as the average of DCF and Relative values:

Valuation History

Warrior Met Coal Inc

Fundamental Analysis

Revenue & Expenses Breakdown

Warrior Met Coal Inc

Balance Sheet Decomposition

Warrior Met Coal Inc

| Current Assets | 887.1m |

| Cash & Short-Term Investments | 506.2m |

| Receivables | 141.6m |

| Other Current Assets | 239.3m |

| Non-Current Assets | 1.7B |

| Long-Term Investments | 44.6m |

| PP&E | 1.6B |

| Other Non-Current Assets | 38.1m |

Free Cash Flow Analysis

Warrior Met Coal Inc

| USD | |

| Free Cash Flow | USD |

Earnings Waterfall

Warrior Met Coal Inc

|

Revenue

|

1.5B

USD

|

|

Cost of Revenue

|

-1.1B

USD

|

|

Gross Profit

|

472.5m

USD

|

|

Operating Expenses

|

-217.1m

USD

|

|

Operating Income

|

255.4m

USD

|

|

Other Expenses

|

-4.8m

USD

|

|

Net Income

|

250.6m

USD

|

HCC Profitability Score

Profitability Due Diligence

Warrior Met Coal Inc's profitability score is 67/100. The higher the profitability score, the more profitable the company is.

Score

Warrior Met Coal Inc's profitability score is 67/100. The higher the profitability score, the more profitable the company is.

HCC Solvency Score

Solvency Due Diligence

Warrior Met Coal Inc's solvency score is 85/100. The higher the solvency score, the more solvent the company is.

Score

Warrior Met Coal Inc's solvency score is 85/100. The higher the solvency score, the more solvent the company is.

Wall St

Price Targets

HCC Price Targets Summary

Warrior Met Coal Inc

According to Wall Street analysts, the average 1-year price target for

HCC

is 73.44 USD

with a low forecast of 62.62 USD and a high forecast of 90.3 USD.

Dividends

Current shareholder yield for HCC is

.

Shareholder yield represents the total return a company provides to its shareholders, calculated as the sum of dividend yield, buyback yield, and debt paydown yield. What is shareholder yield?

The intrinsic value of one

HCC

stock under the Base Case scenario is

71.9

USD.

Compared to the current market price of 49.35 USD,

Warrior Met Coal Inc

is

Undervalued by 31%.

You don't have any saved screeners yet

You don't have any saved screeners yet