Hyundai Heavy Industries Co Ltd

KRX:329180

| US |

|

Johnson & Johnson

NYSE:JNJ

|

Pharmaceuticals

|

| US |

|

Berkshire Hathaway Inc

NYSE:BRK.A

|

Financial Services

|

| US |

|

Bank of America Corp

NYSE:BAC

|

Banking

|

| US |

|

Mastercard Inc

NYSE:MA

|

Technology

|

| US |

|

UnitedHealth Group Inc

NYSE:UNH

|

Health Care

|

| US |

|

Exxon Mobil Corp

NYSE:XOM

|

Energy

|

| US |

|

Pfizer Inc

NYSE:PFE

|

Pharmaceuticals

|

| US |

|

Palantir Technologies Inc

NYSE:PLTR

|

Technology

|

| US |

|

Nike Inc

NYSE:NKE

|

Textiles, Apparel & Luxury Goods

|

| US |

|

Visa Inc

NYSE:V

|

Technology

|

| CN |

|

Alibaba Group Holding Ltd

NYSE:BABA

|

Retail

|

| US |

|

3M Co

NYSE:MMM

|

Industrial Conglomerates

|

| US |

|

JPMorgan Chase & Co

NYSE:JPM

|

Banking

|

| US |

|

Coca-Cola Co

NYSE:KO

|

Beverages

|

| US |

|

Walmart Inc

NYSE:WMT

|

Retail

|

| US |

|

Verizon Communications Inc

NYSE:VZ

|

Telecommunication

|

Utilize notes to systematically review your investment decisions. By reflecting on past outcomes, you can discern effective strategies and identify those that underperformed. This continuous feedback loop enables you to adapt and refine your approach, optimizing for future success.

Each note serves as a learning point, offering insights into your decision-making processes. Over time, you'll accumulate a personalized database of knowledge, enhancing your ability to make informed decisions quickly and effectively.

With a comprehensive record of your investment history at your fingertips, you can compare current opportunities against past experiences. This not only bolsters your confidence but also ensures that each decision is grounded in a well-documented rationale.

Do you really want to delete this note?

This action cannot be undone.

| 52 Week Range |

109 600

269 500

|

| Price Target |

|

We'll email you a reminder when the closing price reaches KRW.

Choose the stock you wish to monitor with a price alert.

|

|

Johnson & Johnson

NYSE:JNJ

|

US |

|

|

Berkshire Hathaway Inc

NYSE:BRK.A

|

US |

|

|

Bank of America Corp

NYSE:BAC

|

US |

|

|

Mastercard Inc

NYSE:MA

|

US |

|

|

UnitedHealth Group Inc

NYSE:UNH

|

US |

|

|

Exxon Mobil Corp

NYSE:XOM

|

US |

|

|

Pfizer Inc

NYSE:PFE

|

US |

|

|

Palantir Technologies Inc

NYSE:PLTR

|

US |

|

|

Nike Inc

NYSE:NKE

|

US |

|

|

Visa Inc

NYSE:V

|

US |

|

|

Alibaba Group Holding Ltd

NYSE:BABA

|

CN |

|

|

3M Co

NYSE:MMM

|

US |

|

|

JPMorgan Chase & Co

NYSE:JPM

|

US |

|

|

Coca-Cola Co

NYSE:KO

|

US |

|

|

Walmart Inc

NYSE:WMT

|

US |

|

|

Verizon Communications Inc

NYSE:VZ

|

US |

This alert will be permanently deleted.

Hyundai Heavy Industries Co Ltd

DCF Value

This DCF valuation model was created by

![]() Alpha Spread

and was last updated on

Dec 23, 2024.

Alpha Spread

and was last updated on

Dec 23, 2024.

Estimated DCF Value of one

329180

stock is

228 746.88

KRW.

Compared to the current market price of 269 500 KRW, the stock is

Overvalued by 15%.

Present Value Calculation

This block is the starting point of the DCF valuation process. It calculates the present value of a company's forecasted cash flows based on selected operating model. Adjust key parameters like discount rate and terminal growth, and alter inputs such as revenue growth and margins to see their impact on valuation.

DCF Model

Base Case Scenario

Switching the operating model will discard any changes made to the current valuation.

You already have a valuation model for Hyundai Heavy Industries Co Ltd.

Do you want to replace it with the current valuation model?

Do you really want to delete your valuation model? This operation cannot be undone.

DCF Value Calculation

This stage translates the present value into DCF value per share. For firm valuation models, it adjusts present value for debt and assets to derive equity value (skipped if using equity valuation model). Finally, this equity value is divided by the number of shares to determine the DCF value per share.

Present Value to DCF Value

Capital Structure

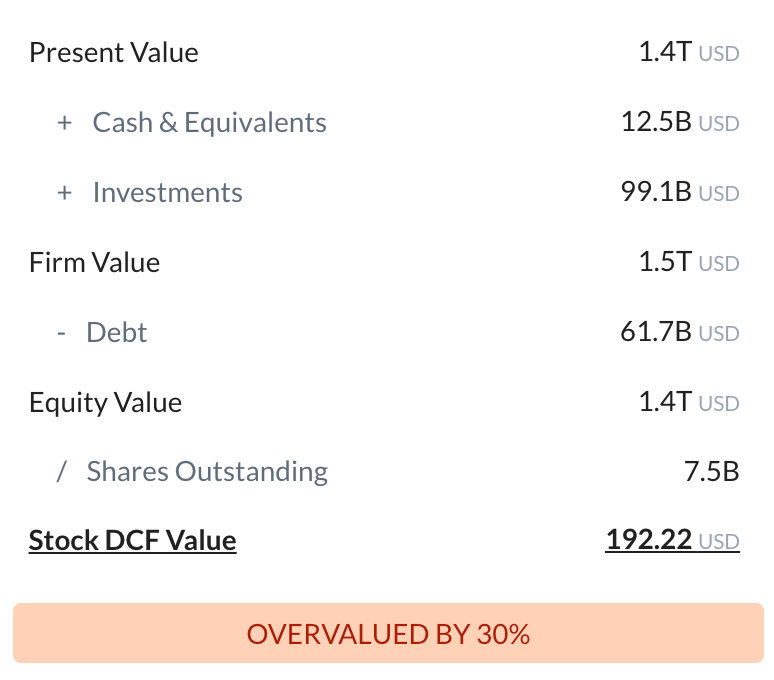

| Present Value | 21.3T KRW |

| + Cash & Equivalents | 928B KRW |

| + Investments | 144.3B KRW |

| Firm Value | 22.3T KRW |

| - Debt | 2T KRW |

| - Minority Interest | 228k KRW |

| Equity Value | 20.3T KRW |

| / Shares Outstanding | 88.8m |

| 329180 DCF Value | 228 746.88 KRW |

Valuation Analysis

Sensitivity Analysis

DCF Value Sensitivity Analysis

Sensitivity Analysis assesses how changes in key factors like revenue growth, margin, and discount rate affect a stock's DCF value. By visualizing various scenarios, from significant downturns to optimistic growth, this tool helps you understand potential valuation shifts, aiding in risk assessment and strategic decision-making.

DCF Financials

Financials used in DCF Calculation

What is the DCF value of one 329180 stock?

Estimated DCF Value of one

329180

stock is

228 746.88

KRW.

Compared to the current market price of 269 500 KRW, the stock is

Overvalued by 15%.

The true DCF Value lies somewhere between the worst-case and best-case scenario values. This is because the future is not predetermined, and the stock's DCF Value is based almost entirely on the future of the company. Knowing the full range of possible stock DCF values gives a complete picture of the investment risks and opportunities.

How was the DCF Value calculated?

1. Present Value Calculation.

Utilizing the DCF operating model, Hyundai Heavy Industries Co Ltd's future cash flows are projected and then discounted using a chosen discount rate to determine its Present Value, which is calculated at

21.3T KRW.

2. DCF Value Calculation. The company's capital structure is employed to derive the total Equity Value from the previously calculated Present Value of the cash flow. This Equity Value, when divided by the total number of outstanding shares, yields the DCF Value of 228 746.88 KRW per share.

You don't have any saved screeners yet

You don't have any saved screeners yet