CJ CheilJedang Corp

KRX:097950

DCF Value

This DCF valuation model was created by

![]() Alpha Spread

and was last updated on

Mar 26, 2025.

Alpha Spread

and was last updated on

Mar 26, 2025.

Estimated DCF Value of one

097950

stock is

1 208 694.13

KRW.

Compared to the current market price of 257 500 KRW, the stock is

Undervalued by 79%.

Present Value Calculation

This block is the starting point of the DCF valuation process. It calculates the present value of a company's forecasted cash flows based on selected operating model. Adjust key parameters like discount rate and terminal growth, and alter inputs such as revenue growth and margins to see their impact on valuation.

DCF Model

Base Case Scenario

DCF Value Calculation

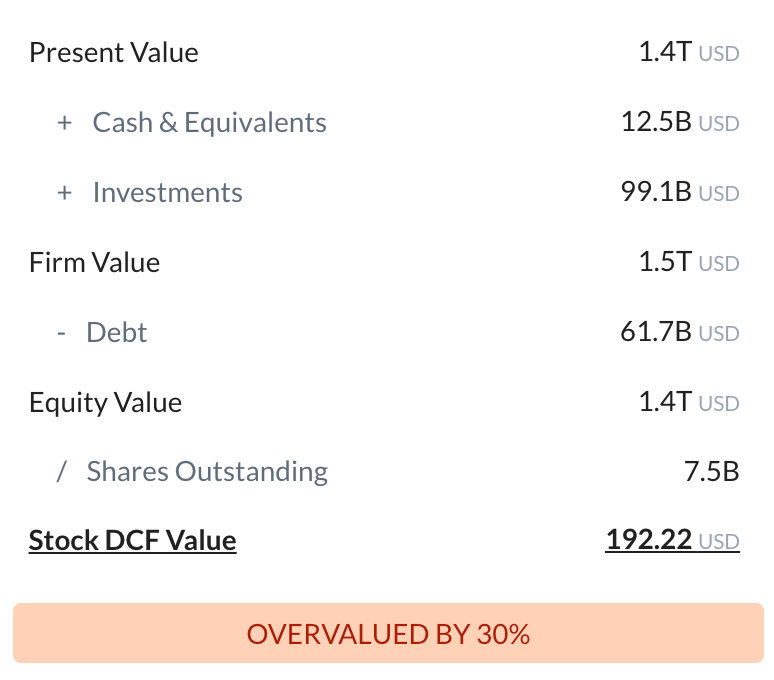

This stage translates the present value into DCF value per share. For firm valuation models, it adjusts present value for debt and assets to derive equity value (skipped if using equity valuation model). Finally, this equity value is divided by the number of shares to determine the DCF value per share.

Present Value to DCF Value

Capital Structure

| Present Value | 19.8T KRW |

| Equity Value | 19.8T KRW |

| / Shares Outstanding | 16.4m |

| 097950 DCF Value | 1 208 694.13 KRW |

You are using the equity valuation model. In this approach, further calculations for converting firm value to equity value are not required. The present value, obtained in the present value calculation block, already represents the equity value.

The DCF value per share is derived by dividing the present value by the number of shares:

Valuation Analysis

Sensitivity Analysis

DCF Value Sensitivity Analysis

Sensitivity Analysis assesses how changes in key factors like revenue growth, margin, and discount rate affect a stock's DCF value. By visualizing various scenarios, from significant downturns to optimistic growth, this tool helps you understand potential valuation shifts, aiding in risk assessment and strategic decision-making.

DCF Financials

Financials used in DCF Calculation

What is the DCF value of one 097950 stock?

Estimated DCF Value of one

097950

stock is

1 208 694.13

KRW.

Compared to the current market price of 257 500 KRW, the stock is

Undervalued by 79%.

The true DCF Value lies somewhere between the worst-case and best-case scenario values. This is because the future is not predetermined, and the stock's DCF Value is based almost entirely on the future of the company. Knowing the full range of possible stock DCF values gives a complete picture of the investment risks and opportunities.

How was the DCF Value calculated?

1. Present Value Calculation.

Utilizing the DCF operating model, CJ CheilJedang Corp's future cash flows are projected and then discounted using a chosen discount rate to determine its Present Value, which is calculated at

19.8T KRW.

2. DCF Value Calculation. The company's capital structure is employed to derive the total Equity Value from the previously calculated Present Value of the cash flow. This Equity Value, when divided by the total number of outstanding shares, yields the DCF Value of 1 208 694.13 KRW per share.

You don't have any saved screeners yet

You don't have any saved screeners yet